Despite a challenging economic climate both at home and abroad, UK investors finished the year in welcome positive territory. The Commercial Team at Santander Asset Management shares their thoughts in the first State of Play of the year.

Did 2023 end back on track?

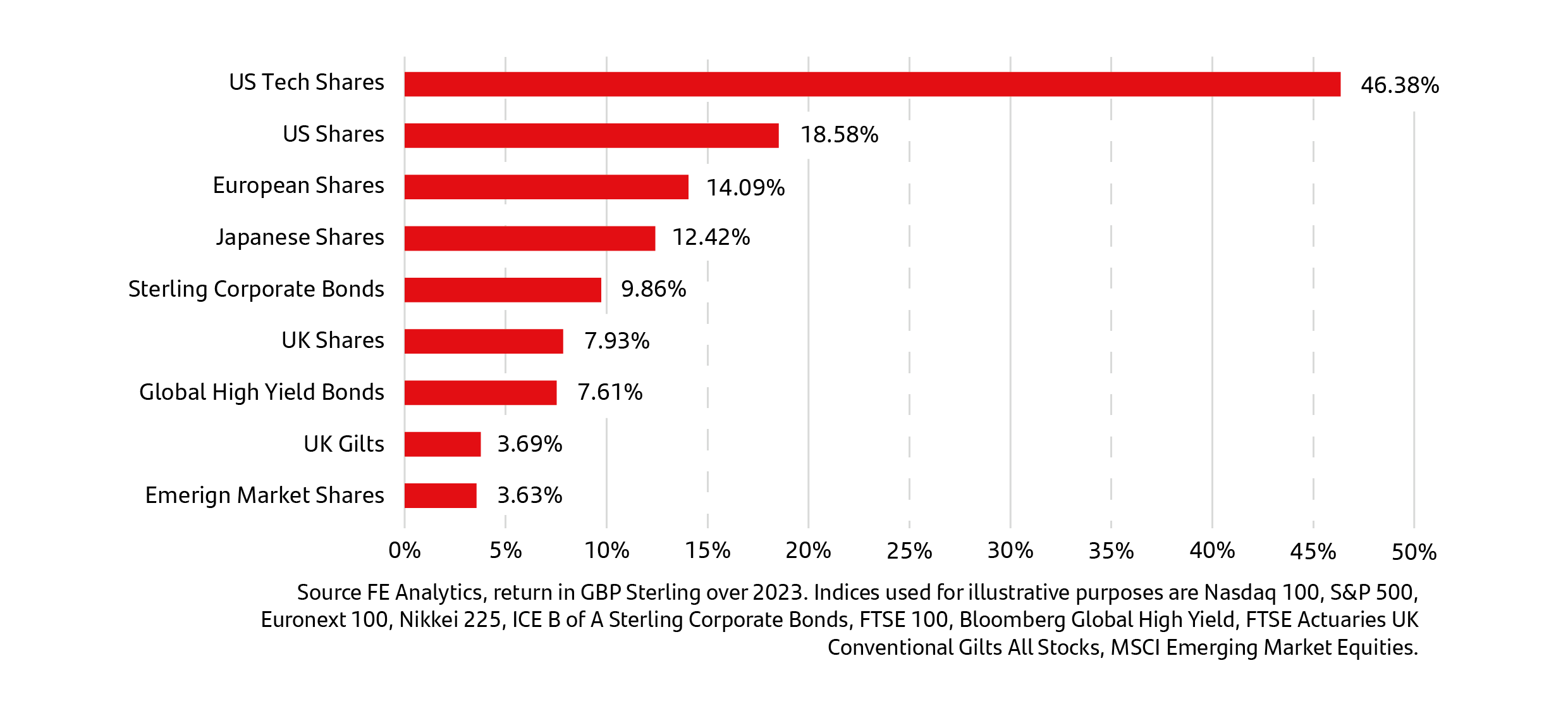

Investors were rewarded for taking on more risk last year, as shares and particularly US tech shares posted the strongest returns. Bond markets also made progress, reversing some of the damage to (lower-risk) portfolio returns we saw in 2022.

Market returns (in £)

A broadly solid economy saw company earnings surprise on the upside, supported by the prospect of an end to the cycle of rising interest rates. Global growth shares (including those in the UK) in particular benefitted from the potential switch in monetary policy from the Federal Reserve and other central banks, alongside a boost from increased enthusiasm for artificial technology.

Investors in bonds were rewarded for their patience, as inflationary pressures eased and the outlook for interest rates improved.

2024 – More of the same?

Over the coming weeks, State of Play will review the key asset classes typically held by investors. In the first State of Play of the year, let’s look at some of the key themes we believe will help to shape markets and investment returns.

Speculation over when central banks will start to lower interest rates is likely to remain a key driver of market sentiment, at least in the first half of 2024. Markets have already begun the year with an intense focus on this area and on the strength of the global economy, as seen in last week’s strong US jobs data.

Inflation is expected to continue to ease throughout 2024, however, a strong labour market is supportive of inflation remaining higher than the 2% target set by many central banks. It is easier to get inflation down from 10% to 5% than it is from 5% to 2%, so we expect inflation to be a hot topic throughout 2024.

Stock markets in 2023 were driven by the strong performance of ‘the magnificent seven’, they are now so large that, according to This is Money, they are worth more than the stock markets of the UK, Japan, France, China and Canada combined1. Will they continue to drive forward? Will the bubble burst or will the concentration risk drive disinvestment? At Santander Asset Management, we have a positive view of shares over the long-term.

Our view is that bonds offer attractive investment opportunities in the current economic environment. The bond market is offering attractive yields relative to historical levels in virtually all segments and geographies. The current levels of investment-grade corporate bond yields are attractive and the quality of company finances in most sectors can withstand an economic slowdown. For the first time in many years, investment-grade bonds offers yields that are competitive with shares.

We expect economic growth to be slow due to the lag effect of higher interest rates, but most economies should avoid a serious recession. Any economies that do suffer a recession will probably see it as short-lived and fairly mild.

Geopolitical events have the potential to throw markets off track. There are unresolved conflicts in Ukraine and Gaza. We have important elections in the UK and the USA. There are also increasing concerns that the USA will be dragged into any conflict between China and Taiwan.

Always remember that one of the few things that we can say with confidence is that 2024 will probably not turn out as expected, which is why a diversified approach to your savings and investments is usually sensible.

Market Update

The first week of trading in 2024 has seen global stock markets ease approximately 1-2%2 , but we should remember that January has historically been a poor month for share returns since 2000. The FTSE All Share Index has only shown gains in 2015, 2019 and 20233. In 2024, markets are also worried about geopolitical events leading to major shipping companies avoiding the Suez canal, adding thousands of miles along with time and cost to global supply chains. This has the potential to add inflationary pressure at a time when markets are debating the timing of central bank rate cuts. The fear is that, at best, this will delay rate cuts and it is not inconceivable that it could even lead to a rate increase if the situation escalates. This is not great for investment markets, as they are looking for reassurance of when rates will fall and anything that could delay that adds uncertainty and brings volatility with it.

The value of seeking guidance and advice

It is important to seek advice and guidance from a professional financial adviser who can help to explain how to build an appropriate financial plan to match your time horizons, financial ambitions and risk comfort. If you already have a plan in place or have already invested, it is important to allocate time to review this to ensure this remains on track and appropriate for your needs.

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 11 January 2024. 1This is Money, 8 January 2024. 2FE Analytics, 8 January 2024. 3Interactive Investor, 8 January 2024.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk