Earlier in 2024, State of Play covered the UK entering a technical recession after two consecutive quarters of negative growth. In the article, we gave our outlook on what was likely to happen next, anticipating that the technical recession would be fairly mild and pass quickly. With new Gross Domestic Product (GDP) figures released for the first two months of 2024, is the UK technical recession expected to be short-lived? Santander Asset Management UK shares their insights in this week’s State of Play.

GDP

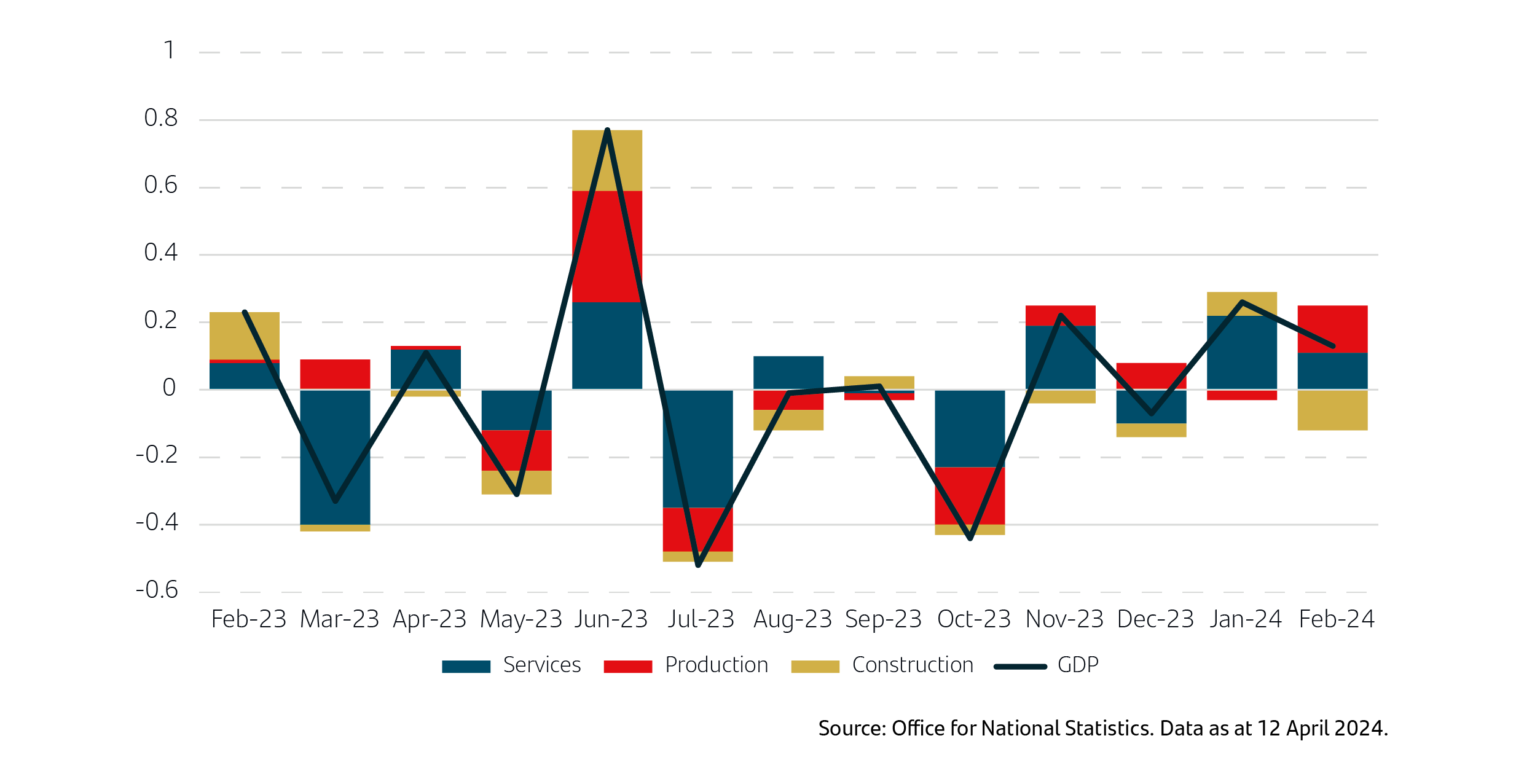

Monthly GDP is estimated to have grown by 0.2% in January and 0.1% in February, following a fall of 0.1% in December 2023. The positive January figure was mainly driven by increasing output in construction and services, particularly retail and wholesaling.1 The February figure was mainly driven by the production sector with a 1.2% rise in manufacturing output.2 The estimations for the quarterly GDP figure are due on the 10 May, however, it is widely forecast that GDP would have grown by 0.3% in the first quarter of 2024.1 With January and February monthly GDP estimates already being positive, it looks like the UK technical recession is already over, although the UK will officially remain in a technical recession until the Office for National Statistics announces its quarterly estimation.

Contributions to monthly GDP growth UK, February 2023 to February 2024

Source: The Economist, 11 April 2024

This will be welcome news for investors in the UK. With economic growth being near zero since 2022, the UK is predicted to end this period of stagnant growth and enter into a longer-term trend of low but stable economic growth. Oxford Economics has recently improved their forecast for 2024 economic growth in the UK to 0.6% from 0.5%. They also expect the economy to grow by 2% in 2025, with consumers leading the recovery due to much lower inflation, boosting spending power.3

Part of the reason the UK economy is expected to grow at a low and stable rate is the lagged impact of interest rate rises by the Bank of England (BoE). Rising interest rates make mortgages more expensive and reduce the amount of money consumers have to spend, this then acts as a way of bringing inflation down as spending cools. The reason this is lagged is because many homeowners will already be on fixed-term mortgages. Homeowners with a mortgage usually lock in a fixed rate deal for two to ten years, meaning that after this period runs out, they will need to renegotiate this loan at the new higher rate and will then have less money in their pocket.

Inflation and wage growth

UK inflation eased to the lowest levels of price rises in almost two and a half years, according to research from the British Retail Consortium. Annual shop price inflation was 0.8% in April, down from 1.3% in March, with the most notable falls due to promotions on clothing and footwear, and fresh food products. Non-food price inflation even turned negative, with deflation of 0.6% in the month, down from 0.2% and the lowest since October 2021.4

Research from Oxford Economics shows that private sector wage growth is predicted to slow sharply in March and April. If official data matches these predictions and inflation continues to fall, it should keep the BoE’s Monetary Policy Committee on track to cut interest rates in the summer. This would then make mortgages and loans cheaper, meaning consumers will have more money to spend, encouraging further economic growth, albeit with a lagged effect due to fixed-term agreements.

FTSE 100 performing well

The FTSE 100 Index, which contains 100 of the most highly capitalised blue-chip companies listed on the London Stock Exchange, has performed well over the last two months, posting monthly gains of 2.4% and 4.2% in April and March, respectively.5 Inflation in the US is proving hard to tame and the US Federal Reserve (Fed) is likely going to take a different route to the BoE and European Central Bank in cutting interest rates. The positive outlook for interest rate cuts in the UK has been part of the reason behind the rise in the FTSE 100 Index in recent weeks. If the interest rate cuts in the US are delayed further, this could draw investors away from the US to the UK stock market, as UK consumer spending is likely to increase earlier than in the US. Typically, when a countries economy enters a recession, it's natural for investors to worry and share prices can fall. The recent FTSE 100 performance shows that the index was not impacted by the announcement and investors were focussed on the overall fundamentals.

Remember why you invested

Although hearing the news that the UK has entered a technical recession was unsettling for some, with media outlets providing a lot of short-term noise, it is always worth remembering why you invested and what your long-term goals are. Since the announcement, the economy has returned to growth and is predicted to grow steadily, UK inflation is continuing to drop with a positive outlook for interest rate cuts going forward, and the FTSE 100 has posted two months of positive gains. If you do feel unsettled during your investment journey, it is important to seek advice and guidance from a professional financial adviser.

Investing can feel complex and overwhelming, but our educational insights can help you cut through the noise. Learn more about the Principles of Investing here.

Note: Data as at 2 May 2024. 1National Institute of Economic and Social Research, 13 March 2024, 2Office for National Statistics, 12 April 2024, 3Oxford Economics, 22 April 2024, 4Proactive Investors, 30 April 2024, 5Reuters, 30 April 2024.

Important information

For retail distribution.

This document has been approved and issued by Santander Asset Management UK Limited (SAM UK). This document is for information purposes only and does not constitute an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Opinions expressed within this document, if any, are current opinions as of the date stated and do not constitute investment or any other advice; the views are subject to change and do not necessarily reflect the views of Santander Asset Management as a whole or any part thereof. While we try and take every care over the information in this document, we cannot accept any responsibility for mistakes and missing information that may be presented.

The value of investments and any income is not guaranteed and can go down as well as up and may be affected by exchange rate fluctuations. This means that an investor may not get back the amount invested. Past performance is not a guide to future performance.

All information is sourced, issued, and approved by Santander Asset Management UK Limited (Company Registration No. SC106669). Registered in Scotland at 287 St Vincent Street, Glasgow G2 5NB, United Kingdom. Authorised and regulated by the FCA. FCA registered number 122491. You can check this on the Financial Services Register by visiting the FCA’s website www.fca.org.uk/register.

Santander and the flame logo are registered trademarks.www.santanderassetmanagement.co.uk